What Is a Business Loan? A Complete Guide for Beginners

Introduction

In today’s competitive market, starting or growing a business often requires more money than an entrepreneur currently has. Whether it’s launching a new idea, expanding operations, purchasing equipment, or strengthening cash flow, businesses rely heavily on financial support. One of the most common sources of this support is the business loan.

A business loan is more than just borrowing money—it is a strategic financial tool that helps companies manage growth, overcome challenges, and reach long-term goals. In this comprehensive guide, we will explain what a business loan is, how it works, its types, benefits, risks, and how to choose the right loan for your business. By the end of this article, you’ll understand everything you need to know before applying for one.

What Is a Business Loan?

A business loan is money that companies borrow to use for many different purposes. Money can be borrowed from banks, financial institutions or online lenders. The loan will have to be paid back over time with interest.

Some examples of what the loan can be used for include

- To establish a new business

- To pay for day-to-day (operational) expenses

- To purchase equipment and/or inventory.

- To add locations/branches to an existing business

- To hire staff

- To improve cash flow

- To market or advertise.

Having access to a business loan allows companies the financial flexibility to manage their day-to-day operations and/or expand their current market without experiencing a long wait time until they have the capital on hand needed before starting their operation.

How Do Business Loans Work?

Even though the structure of a business loan is rather simple, different lenders can apply slightly different terms.

Here is a general overview of how they work:

1. Application

An application for a business loan requires the submission of one or more documents, which may include:

- Bank statements

- A business registration certificate

- Financial Reports (balance sheet, profit and loss statement, etc.)

- Identification Documents (ID cards, passports, etc.)

- Tax Returns

- A business plan

2. Evaluation

When a lender evaluates your application for a loan, the lender typically evaluates the following information when deciding whether to approve or decline an application:

- Credit Score

- Total Business Income

- Cash Flow of Your Business

- Total Amount of Debt (Total debt a business owes)

- History of Business Operations

3. Approval & Terms

If a lender is willing to approve an application for a loan, the lender will provide the applicant with loan terms relating to:

- Loan Amount

- Interest Rate

- Repayment Period

- Fees

- Collateral (if needed)

4. Disbursement

Upon acceptance of the terms provided by the lender, the applicant will receive the funds requested.

5. Repayment

Loans to businesses are generally repaid in weekly, monthly, or daily installments, depending on the contract between the lender and the borrower.

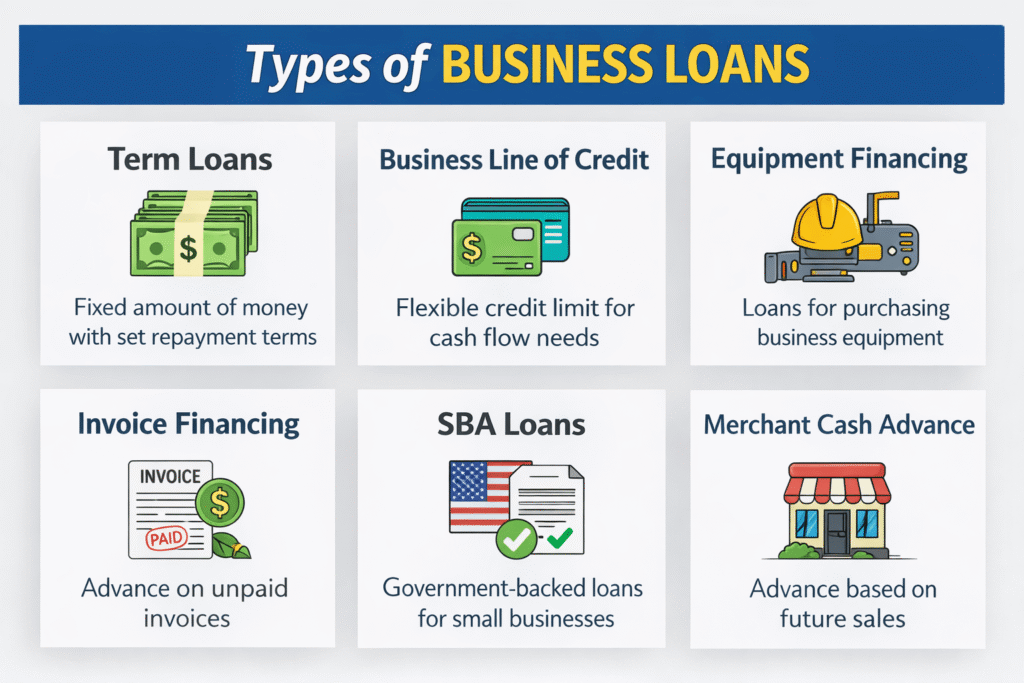

Types of Business Loans

There are many types of business loans available, each with its own purpose. Below are some of the most common types of business loans available:

1.Term Loans

Term loans are short, medium and long term loans that require the borrower to repay a fixed amount of money, usually paid back in monthly payments over a set period of time.

Good For:

- Growing Your Business

- New Equipment Purchases

- Long-term Investments

Types of Term Loans:

- Short-term (12 months or less)

- Medium-term (1-3 years)

- Long-term (3-10 years)

2. Business Lines of Credit

A business line of credit works like a credit card, allowing you to make purchases using a predetermined credit limit, and you will only pay interest on the amount used.

Good For:

- Managing Your Cash Flow

- Unforeseen Expenses

- Seasonal Business Owners

3. Equipment Financing

A loan to purchase equipment such as machinery, vehicles, computers and tools for your business.

- Benefits of Equipment Financing:

- The equipment itself will serve as collateral

- Quick approval times

- Lower interest rates

4. Invoice Financing

Using invoices as collateral, you can borrow against unpaid invoices from customers to cash flow your business.

Good For:

- Companies that have customers who take a long time to pay

- Improve Your Cash Flow

5. SBA Loans (U.S. Government)

SBA loans are backed by the government, making them a lower cost option than traditional bank loans.

Good For:

- Start Ups

- Small Businesses Looking for Financing at a Low Cost

6. Merchant Cash Advances

A MCA provides money upfront in exchange for a percentage of daily sales.

Best for:

- Businesses with high card transactions

- Need for quick cash

Warning:

These have high fees and should be used carefully.

7. Microloans

These are small loans typically under $50,000 and great for new businesses or entrepreneurs who cannot access traditional loans.

Do Businesses Need Loans?

There are several reasons why businesses get loans:

- Starting a Business – Many entrepreneurs have good ideas but do not have enough money to start their business. Business loans enable these businesses to get started.

- Maintain Cash Flow – Cash flow is the lifeblood of any business. Business loans are designed to allow all kinds of businesses to survive during slow months, unexpected emergencies, and times when customers may not pay on time.

- Expand Operations – Businesses often want to expand into other geographic areas or provide new and different services in their current area. Loans will provide the necessary working capital to:

- Open new locations

- Increase the number of products produced

- Upgrade technology

- Hire additional employees

- Purchase Inventory and Equipment – When companies need to purchase large amounts of equipment, purchasing them outright can be very expensive. Loans will spread the cost of equipment over a longer timeframe.

- Marketing – If a company does not market its business, it will struggle to grow. A business loan will enable the owner or management team to invest in marketing techniques that will help bring in new customers.

- Build Business Credit – Just like an individual, businesses are able to build business credit if they have a history of paying their debts on time. A business loan will assist in creating this credit history.

Pros of Business Loans

- Retain Control of the Business

When using a loan as opposed to an investor, the lender doesn’t take shares of your company.

- Flexible Options for Use

Many lenders will allow the borrower to use the funds for anything they wish.

- Potential Tax Advantages to the Borrower

In some areas of the country, you can deduct the interest you pay on loans from your taxes.

- Fixed Payments and Reliable Budgeting

Because of the fixed time periods associated with loans, managing your business’ finances is easier than without them.

- Potential for Increased Expansion and Efficiency

With the right type of loan, a business can grow at a faster pace and run more efficiently.

Cons of Business Loans

- Loan Costs (Fee and Interest)

Loans require repayment and high rates of interest can strain a business.

- Qualification Process Requires Good Credit History

Businesses that have not established good credit cannot qualify for loans/loans will be much lower than what they would be able to secure with good credit.

- Required Collateral

Some financial lenders require you to pledge your property and/or equipment in order to secure the loan.

- Debt Risk

The failure to repay your loan can result in penalties (monetary and/or other) and/or legal immigration issues.

- Regular Cash Flow Pressure

In order to sustain your cash flow position, it is important that your business generates sufficient income to repay your loan during each repayment period.

How to Qualify for a Business Loan

1. Establish Creditworthiness

A strong credit report lends itself to higher chances of receiving assistance.

2. Gather Financial Documentation

All financial documentation will be required by banks, including:

- Income

- Expenses

- Profitability

3. Write A Business Plan

Lenders will want evidence of your company’s capability for success.

4. Decrease Existing Debt

Less debt translates to less risk for lenders.

5. Obtain the Appropriate Loan

Applying for an inappropriate type of loan will likely result in denial.

Finding The Right Loan

With the plethora of options for loans available to business owners, it may be difficult to select the most appropriate loan. The following steps will assist you in doing so:

1.Define the Reason for Borrowing

Are you looking to borrow money for:

- Expanding Your Existing Business?

- Purchasing Equipment?

- Managing Cash Flow?

- Starting A Business?

Identifying your intended purpose will dictate the type of loan you need.

2. Review Interest Rates

The lower the interest rate, the more money you’ll save.

3. Analyze Payment Terms

Select a payment plan that is most advantageous for your financial situation.

4. Be Aware of Fees

Be aware of:

- Loan origination fee

- Application processing fee

- Overdue payment charges

5.Review The Reputation of The Lending Institution

Choosing to work with endorsed organizations will help you avoid scammers and improprieties.

How to Manage Business Loan Financials Correctly

1. Only Get A Loan For The Amount You Require

Too Much Debt Can Have Negative Consequences For Your Business.

2.Track Incoming Cash Flow

Be Able To Pay Your Loan Payments In A Timely Manner.

3.Make Additional Payments On Your Loan If Allowed By The Agreement

This Will Help Save You On Interest Expense On Your Loan.

4.Avoid Taking Out Multiple Loans At The Same Time

Too Much Debt Increase The Financial Risk To The Business.

5.Use Loans For Business Purpose Only

Use Loans To Help Fund Business Activities That Will Grow Your Business Rather Than For Personal Expenses.

Borrowing using a Business or Personal Loan: How are they different?

– Business Loans

- Can be used only for the business

- Require documents specific to the business e.g. Business Plan and copies

- Amounts can be significant

- Will build your Business Credit

- Many require collateral

– Personal Loans

- Can use your personal (non-business) credit history

- Amounts can be much smaller than a business loan

- Interest can be much higher than a business loan

- Do not have to provide documentation which proves the success of your business

Using a Personal Loan as a means of financing Business is doable but was highly risky as you will be legally responsible for the payments.

Business Loan Myths

- Big Companies are the only ones who will be granted a Business Loan Thousands of small businesses are approved for loans every year including microloans and loans from new internet based lenders.

- You Have To Have Been Profitable Some lenders will consider your potential, and not just your current profits, when determining whether to grant you a loan.

- Your Credit Must Be Perfect Good credit is a great asset to have when applying for a loan, but it may not always be an obligation to have perfect credit to be approved for a loan.

- Only Businesses needing Cash Will Receive Loans Many profitable businesses use loans to grow their business or open new lines of business.

Conclusion

A business loan is one of the most powerful financial tools available to entrepreneurs. Whether you are launching a startup, expanding operations, improving cash flow, or purchasing equipment, a business loan can provide the financial support you need to reach your goals.

However, like any financial decision, it must be approached with planning, understanding, and responsibility. Knowing the types of loans, their benefits, risks, and how to qualify will help you make smarter decisions that support long-term business success.

If you use a business loan wisely, it can guide your business toward growth, stability, and profitability.