What Is a Loan? How It Works and the Different Types

A loan is an amount of money that one person, bank, or institution gives to another person with the agreement that the money will be paid back later, usually with an extra amount called interest. In simple words, a loan is borrowed money that must be returned over time according agreed terms. People and businesses take loans when they need money for something important such as buying a house, starting a business, paying school fees, or handling an emergency but do not have enough cash at the moment.

In today’s financial world, loans play a major role in helping people and businesses achieve their goals. Whether it’s buying a home, paying for education, starting a business, or handling an emergency, loans provide access to money that can be paid back over time. Understanding what a loan is, how it works, and the different types available can help you make smarter financial decisions.

What Is a Loan?

A loan is a financial agreement between a lender and a borrower where the lender advances an amount of money to the borrower with the expectation that it will be paid back over time, typically through monthly payments that also include interest charged on the loan.

Loans are made up of several key pieces:

- The total amount of money that is lent/borrowed (the principal).

- The interest rate (the cost of borrowing money).

- The term of the loan (the amount of time that the borrower must repay the loan).

- The repayment schedule (the frequency with which the borrower makes payments on the loan).

- The lender (the institution or individual who gives you the money).

- The borrower (the person receiving the loan and who is obligated to pay it back).

How Does a Loan Work?

There are four basic steps involved in obtaining a loan.

Step 1: Create an Application

The first step to getting a loan is applying for one. The borrower must complete an application. This includes providing the lender with the borrower’s personal information including their income, employment record and credit history.

Step 2: Get Your Loan Approved

After completing the application and submitting it, the lender will then review it to determine if the applicant is able to repay the loan. The lender determines the borrower’s repayment ability based on several factors including the borrower’s credit score, the borrower’s income, and any other outstanding that the borrower has.

Step 3: Receive Loan Terms

After the lenders determines that the borrower will be able to repay the loan, they then provide the borrower with information about the loan including:

- The amount of money to be borrowed.

- The interest rate that will be charged.

- The length of the loan.

- The monthly payment amount.

Step 4. Receiving the Money

After agreeing to the terms, the borrower receives the funds. This might be directly into their account or paid to a third party (like in home or car loans).

Step5. Repayment

The borrower repays the loan over time. If payments are late or missed, penalties may apply, and credit scores can be affected.

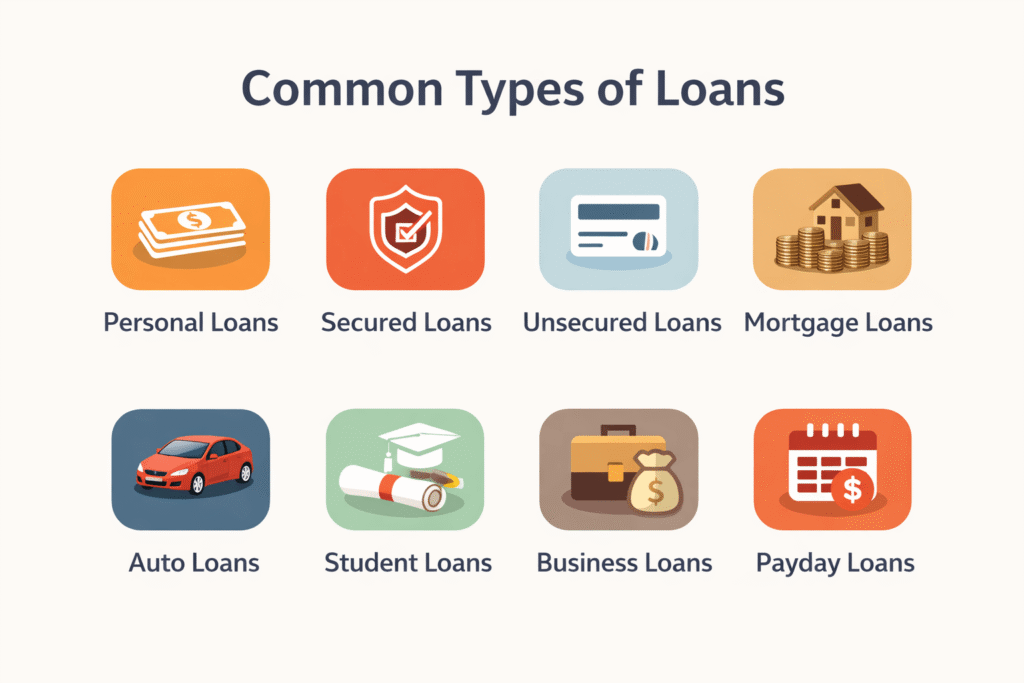

Common Types of Loans

Loans are available in many varieties based on their intended uses and their structure. Here are the most typical categories of loans:

1. Personal Loans

Unsecured loans can be used for virtually anything (medical bills, travel, home improvement, etc.). The following characteristics apply to personal loans:

- No collateral required

- Higher interest than secured loans

- Can be used for many different purposes

2. Secured Loans

Secured loans require collateral (an asset such as a car, house, or savings account). If the borrower does not repay the secured loan, the lender can seize the asset. Some examples of secured loans include:

- Car loans

- Mortgages

3. Unsecured Loans

Unsecured loans do not require collateral. They are reliant mainly on the borrower’s credit and income. Examples of unsecured loans include:

- Personal loans

- Credit cards

4. Mortgage Loans

Mortgage loans are used solely for purchasing a home or piece of property. They also typically have long repayment terms (15 – 30 years) and lower interest rates as the home will be used as collateral.

5. Auto Loans

Auto loans are used to purchase a car, truck, motorcycle, etc. and are secured by the vehicle itself. The term for an auto loan is medium-range (3 – 7 years).

6. Student Loans

Student loans can come in both government and private forms and are designed for education-related expenses such as tuition, textbooks, and housing. Government loans typically offer borrowers a lower interest rate.

7. Business Loans

To facilitate growth, finance expenses, or invest in their operation, businesses will seek a variety of loan types, including:

- Startup loans

- Equipment loans

- Commercial real estate loans

8. Payday Loans

Payday loans are short-term loans that help cover an expense until the paychecks are received by the borrower.

Why Do People Take Loans?

In today’s economy, it is nearly impossible to go without using a loan. Most people do not have enough money to buy large-ticket items like homes, cars, or tuition fees at once. Loans provide an opportunity for individuals to do the following:

- Purchase an asset now and pay for it later.

- Start or grow a business.

- Pay for unexpected costs due to emergencies.

- Invest in education for themselves or a family member.

- Resolve temporary financial problems.

If there were no loans available, many people would put their dreams and opportunities on hold for several years.

Advantages of Borrowing Money

- You will have instant access to cash

- Improves credit history

- Financing large items is easy

- Options for how and when you repay

Disadvantages of Borrowing Money

- Very high interest charges for low/poor credit

- Can easily go over budget

- You run the chance of losing what you put up as collateral

- Costs from late payment or defaulting can really add up

Conclusion

Understanding how loans work is essential for making smart financial decisions. A loan can be a powerful tool to help you reach goals—if you choose the right type and understand the terms. Always compare offers, check interest rates, and only borrow what you can afford to repay.